THE WEAKEST LINKS: US Banks Where Wire Checks Face the Least Scrutiny

Yesterday I gave you the blueprint for getting wire checks accepted. Today, we’re getting specific about the US market.

Because here’s the reality: not all American banks have their act together. Some have been hit with massive fines for compliance failures. Others have admitted to processing hundreds of millions in suspicious transactions. And some are so behind on fraud detection technology that they won’t catch anything sophisticated.

Let’s break down the US institutions where your wire check faces the lowest scrutiny.

The Major Banks With Major Compliance Failures

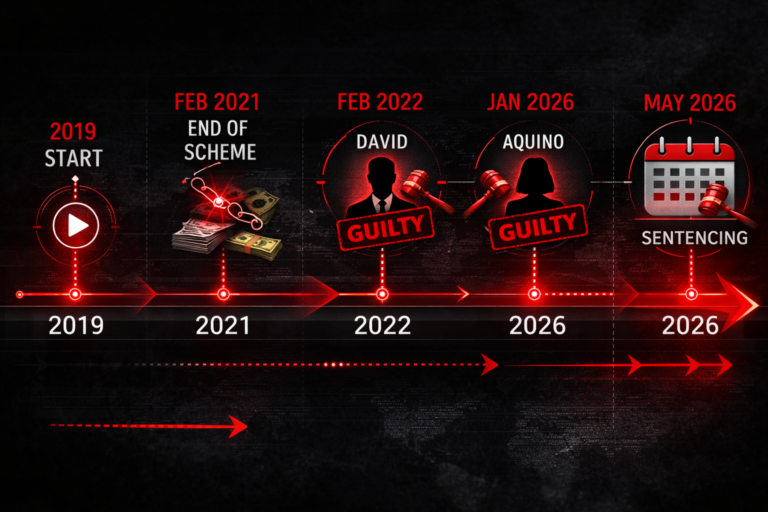

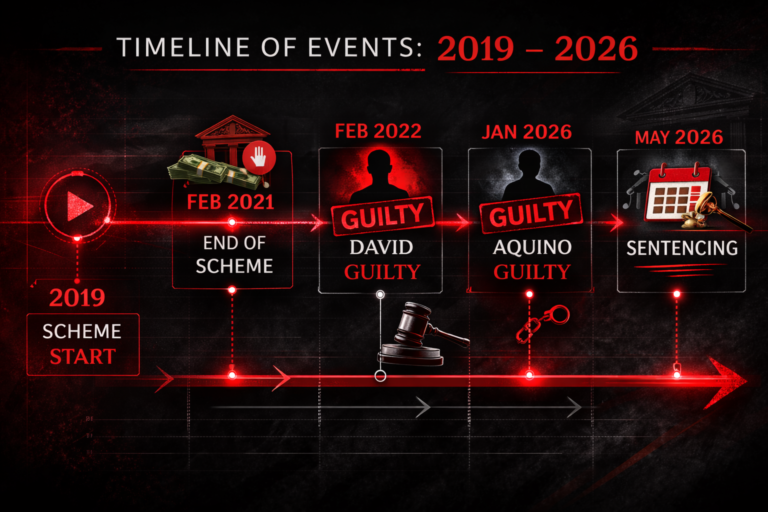

Why it’s weak: In January 2026, a former TD Bank employee pleaded guilty to facilitating a money laundering network that moved hundreds of millions through TD accounts.

The details are staggering:

The network moved nearly $500 million through TD Bank accounts

The insider processed approximately 1,680 official bank checks totaling more than $92 million

Nearly all checks were funded with cash deposits exceeding $10,000

The employee deliberately failed to identify the money launderer on Currency Transaction Reports

What this means for you: When a bank’s own employees are actively helping criminals evade detection, their compliance systems are compromised. TD Bank has demonstrated that insider threats exist and their oversight failed spectacularly. If they missed nearly $100 million in suspicious official checks, what else are they missing?

Risk level: Medium-High (insider corruption creates unpredictable outcomes)

Digital Platforms With Systemic Failures

Cash App (Block, Inc.)

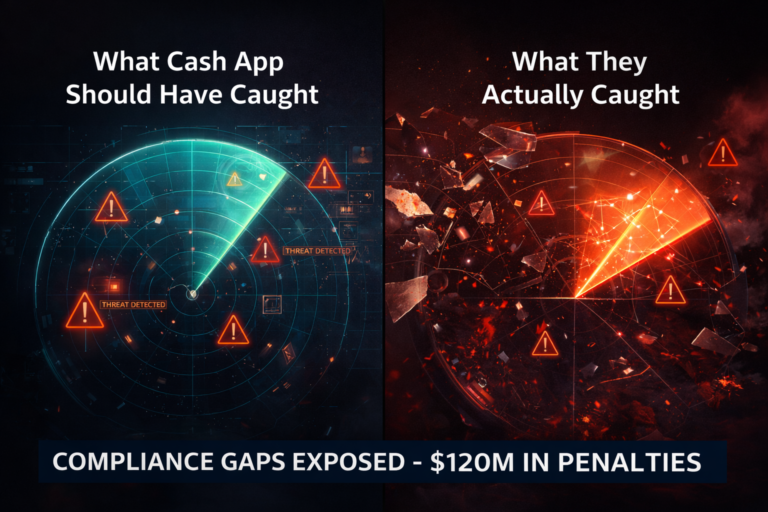

Why it’s weak: Cash App has been hit with two massive enforcement actions in the past year totaling over $120 million in penalties.

In January 2025, a multi-state enforcement team (48 states + DC) fined Block, Inc. $80 million for Bank Secrecy Act and Anti-Money Laundering failures. The regulators found that Cash App’s compliance gaps potentially created opportunities for its services to be used in supporting terrorism financing, money laundering, or other illegal activities.

Then in January 2026, New York’s Department of Financial Services hit Cash App with another $40 million penalty for similar failures—inadequate customer due diligence and risk-based controls.

The New York regulator specifically noted that Cash App’s “lax oversight of bitcoin transactions and its subsequent rapid growth created a vulnerable environment, susceptible to criminal exploitation.”

Most damning: Cash App discovered in a 2022 internal investigation that 8,359 accounts were linked to a Russian criminal network.

What this means for you: Cash App isn’t a traditional bank, but it’s a massive financial platform. Their compliance culture has been repeatedly exposed as inadequate. When a platform admits they had over 8,000 accounts tied to Russian criminals, their detection systems have obvious gaps.

Risk level: High

Credit Unions: The Overlooked Vulnerabilities

Credit unions present a unique opportunity—and I’ll explain why.

The Fraud Resolution Gap

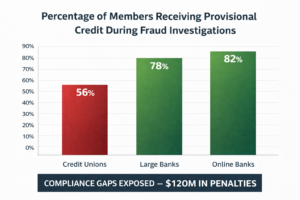

Research from Cornerstone Advisors shows that while credit unions excel at detecting fraud, they lag significantly in resolving it. Only 56% of credit union members receive provisional credit during fraud investigations—the lowest rate among all financial institutions

The digital experience gap is even worse: 82% of credit union members reported that digital document upload was unavailable during their fraud experience. Members are forced into outdated processes—mailing documents, visiting branches, or waiting on hold.

What this means for you: Credit unions have outdated, manual processes. When members can’t even upload documents digitally, you can bet their check verification systems aren’t cutting-edge either. Manual review means human error. Human error means opportunities.

The Compliance Resource Problem

Credit unions consistently struggle with compliance resources. Many lack the budget for sophisticated fraud detection systems. They’re still dealing with basic issues like Regulation E compliance (unauthorized transactions), Regulation Z (lending disclosures), and Regulation V (credit reporting errors).

When a credit union is worried about getting sued over improper overdraft fees, they’re not investing in the latest check verification technology.

The Call Authentication Gap

Here’s something most people don’t consider: credit unions are particularly vulnerable to phone-based verification fraud. Industry groups recently warned the FCC that current call authentication frameworks are failing to protect credit union members.

Many calls still pass through legacy networks that strip authentication data, leaving credit union members vulnerable to scammers posing as their financial institution.

The Regulatory Landscape: Why Some Banks Are Weaker Than Others

The Deregulation Push

In February 2026, Senators Elizabeth Warren and others called on the OCC and FDIC to rescind a proposed rule that would “weaken enforcement and supervisory tools, paving the way for more bank failures.”

The proposed rule would make it harder for examiners to take action against banks—requiring that harm be “likely” (not just possible) and “material.”

What this means for you: If regulators have fewer tools to police banks, some institutions will become less vigilant. The oversight is loosening at exactly the wrong time.

AML Enforcement Is Down (Temporarily)

AML Enforcement Is Down (Temporarily)

Fenergo’s annual report shows that US AML penalties fell by 61% in 2025, driven largely by workforce shifts and constrained enforcement capacity. The US issued only 31 fines in 2025, down 34% from 47 in 2024.

But here’s the key: the report notes this reflects “operational and capacity challenges rather than any easing of regulatory expectations.” Once capacity returns, enforcement will follow.

What this means for you: Right now, regulators are understaffed. That means less oversight of banks. Less oversight means weaker compliance enforcement. The window won’t last forever.

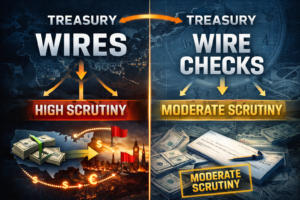

Treasury's New Fraud Initiative

On January 9, 2026, Treasury Secretary Scott Bessent announced new federal actions targeting fraud, with banks placed “squarely on the front lines to detect and deter financial fraud.”

FinCEN has issued targeted alerts identifying red flags, specifically targeting international wires and pass-through transfers that move funds quickly.

What this means for you: Treasury is watching wires specifically. Wire checks? Different category. But the heightened scrutiny means some banks will tighten up. Others will lag behind.

The Nacha ACH Rules: A Distraction for Banks

Here’s something interesting: starting March 2026, Nacha’s new ACH fraud monitoring rules take effect. These rules require risk-based fraud detection at every stage—from onboarding to payment execution.

The problem: 80% of financial institutions are still unprepared or unsure of compliance needs. Experts warn that many firms risk falling behind, and legacy systems are unlikely to meet new fraud detection expectations.

What this means for you: Banks are scrambling to meet ACH compliance deadlines. Their attention and resources are focused on ACH monitoring, not check verification. While they’re upgrading ACH systems, check verification remains an afterthought.